Account-to-account (A2A) payments represent a foundational shift in the way financial transactions are conducted globally. At the heart of the A2A ecosystem are key players that include financial institutions, payment processors, and fintech companies, all of whom work together to ensure the secure and efficient movement of funds. Together, they provide the infrastructure, security, and regulatory compliance necessary for A2A payments to become a popular and reliable payment option.

With this in mind, let’s take a deeper look at A2A payments to better understand what it is, how it works, challenges and considerations, and how it’s modernizing payments.

What are Account-to-Account Payments?

A2A streamlines the payment process by facilitating the direct transfer of funds from one account to another, bypassing traditional intermediaries such as card networks. A2A payments have existed for some time, but recent technological enhancements have spearheaded their growth and appeal as a preferred payment method.

Modern A2A payments are made directly from one party to another via digital tools on dedicated payment rails, most often instantly. These direct transfers typically result in faster and more cost-effective transactions, a net-benefit for both parties involved.

A2A payments are most commonly associated with bank account payments, such as when a consumer uses a bank transfer or direct debit to pay a bill. In Canada, bank account payments are also known as Electronic Fund Transfer (EFT) payments, while in the United States they’re known as Automated Clearing House (ACH) payments. With advances in technology, A2A payments can now support all direct account payments, including bank and digital wallets.

Open Banking, the development of new payment rails, and consumer preferences growing for A2A payments show its potential to become the payment method of choice for consumers and businesses.

Types of A2A payments

- Push payments: This is the process of manually sending or “pushing” money from one account to another, examples of this include bank transfers and instant payments. APIs or emails with account links can also be used to facilitate push payments by sending customers notifications or prompts.

- Pull payments: This is the process of withdrawing or “pulling” money from one account to put into another. An example of this is a direct debit payment, where consent is provided by the payer for a payment to be “pulled” from their account. This payment type is typically used by businesses with recurring payment models, such as subscriptions or loan repayments.

The Advantages of A2A Payments

With A2A payments gaining popularity, let’s take a look at some of the benefits that come with this payment method:

Reduced Transaction Costs: By eliminating the need for intermediaries such as card networks and processing entities, A2A payments significantly reduce transaction fees. This streamlined approach not only lowers costs for businesses by cutting out middlemen but also benefits consumers thanks to reduced or even eliminated processing fees. The efficiency of A2A payments, therefore, translates into tangible savings, making them an increasingly attractive option for cost-conscious individuals and businesses alike.

Faster Processing Times: Account-to-account payments are synonymous with speed and efficiency. By directly connecting payer and payee accounts, they bypass the layers of processing typically associated with traditional payment methods. This direct route accelerates the payment process and also ensures that funds are available more swiftly. For businesses, this can improve cash flow and operational efficiency, while for consumers, it means quicker access to their funds. In an era where convenience is paramount, A2A payments provide a significant advantage for both sides.

Enhanced Security Features: Enhanced security features are pivotal in safeguarding financial transactions. By directly linking two accounts, these payments minimize the exposure to potential fraud that can occur with intermediary handling. The security protocols of financial institutions, together with advanced encryption and authentication measures, strengthen the transaction against unauthorized access. Moreover, the reduced number of transaction touchpoints inherently decreases the risk of data breaches.

Streamlined User Experience: A2A simplifies transactions, allowing users to bypass the disjointed steps often associated with traditional payment systems. With fewer screens to navigate and no need to enter card details or wait for third-party approvals, users enjoy a frictionless payment journey. This ease of use enhances customer satisfaction while also encouraging repeat transactions, creating a better overall experience for all parties involved.

Direct Integration with Financial Institutions: Direct integrations with financial institutions facilitate real-time data exchange and immediate transaction validation, which streamlines the payment process. For businesses, this means they can reconcile accounts faster and manage their finances more effectively. Customers enjoy a more reliable and transparent transaction experience, with the added reassurance that their financial data is handled securely within the trusted infrastructure of their banking institutions.

The Role of Open Banking in A2A Payment Innovation

Open Banking has completely changed the game for A2A payments. Before Open Banking, A2A did not offer any significant benefits over using cards or other payment methods. User experiences were disjointed; first time payment setups required one-off payments to start, manual bank transfers required payers to log into their bank accounts every time they wanted to make a payment, recurring payments often required long authorization forms and so on.

In fact, Canadians pay some of the highest interchange fees ("swipe fees") in the world, which cuts into businesses' profit margins. For example businesses often pay 1.5% to 3.0% of the total transaction value with credit cards. Wire transfers or bank drafts, although secure, can also be expensive and take between 3 to 14 days be processed. Without better alternatives, businesses have accepted the high card processing fees and delayed reconciliation times.

The simplicity and ease of use offered by Open Banking APIs has propelled the growth of A2A payments. With Open Banking, APIs connect a financial institution with third-party applications or other financial services, enabling the user to provide their consent for the direct movement of data or money. These APIs also facilitate the interoperability and secure exchange of financial data and payment initiation outside of financial institutions.

This means that A2A payments can now be made at the point of purchase, offering speed, convenience, and a unified user experience without reliance on card processing fees, excessive data entry or delayed transfers.

Challenges and Considerations

Addressing Fraud and Security Concerns

A2A payments, while offering convenience and efficiency, also present certain fraud and security concerns. Fraudsters may exploit vulnerabilities in the system to conduct unauthorized transactions, identity theft, or even initiate phishing attacks. This is why it's crucial for financial institutions and payment service providers to implement robust security measures to counter these concerns. This can include multi-factor authentication, encryption technologies, real-time transaction monitoring, and regular system audits. Doing so will ensure the highest level of security and maintain the trust and confidence of users in A2A payments.

Overcoming Resistance from Traditional Payment Providers

Obviously, credit card companies and third-party payment payment providers are going to be resistant to a competitive payment method that would cause them to lose revenue. Overcoming resistance from traditional payment providers towards A2A payments requires a strategic approach. Traditional providers may be hesitant due to concerns about security, fraud, and the potential disruption of established systems. To address these concerns, it's essential to demonstrate the benefits of A2A payments, such as cost-effectiveness, speed, and convenience for customers. By effectively communicating these advantages and implementing strong security protocols, resistance from traditional payment providers can be mitigated.

Ensuring Accessibility and Inclusivity

By allowing direct transfers between accounts, A2A payments do not rely on physical banking infrastructure to operate, making financial services more accessible to those in remote or underserved areas. Additionally, these payment methods often require only a basic smartphone or internet connection, making them inclusive for individuals who may not have access to traditional banking systems. A2A payments can also be more cost-effective, removing financial barriers and promoting greater participation in the digital economy.

The Future of A2A Payments

In Canada, the top three payment methods most used by Canadian consumers for online purchases have been credit cards, debit cards and online payment services. This shows A2A’s growth potential in Canada, as many consumers are already familiar with and using these types of online payment methods. The existing market trend towards digital transactions provides a promising landscape for A2A to expand its services and gain a significant customer base.

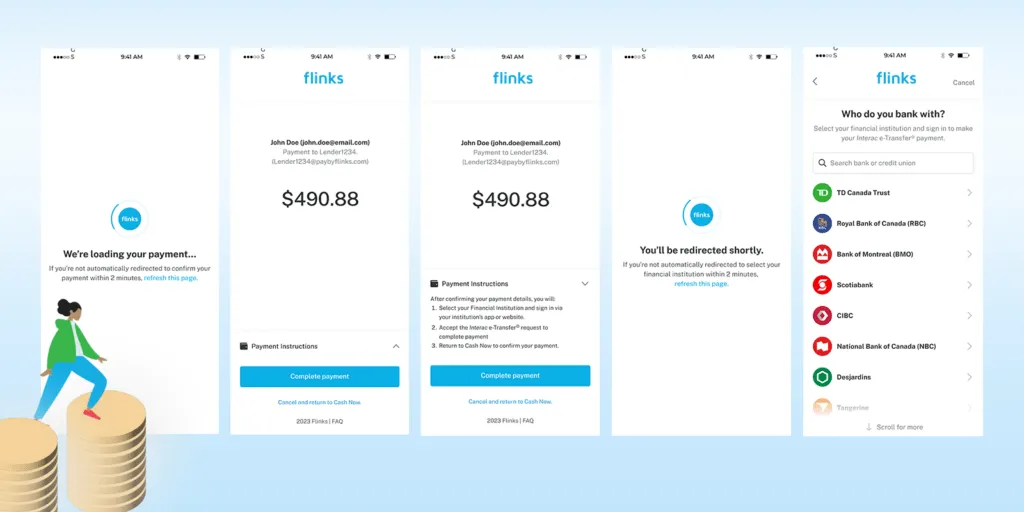

Flinks Pay is a prime example of a Canadian fintech anticipating the evolving needs of Canada’s payment market. With Canada seeing a broader transition from traditional payments such as cheques to digital payments (such as EFTs and Interac™ e-transfers), Flinks just launched an A2A solution that streamlines the payment process for consumers and businesses alike. By enabling reliable instant payments within one unified product flow, Flinks Pay is a seamless and efficient payment solution that will transform the Canadian payment landscape by reducing reliance on credit cards and eliminating the need for micro-deposits for businesses and consumers.

Innovation in North American payments is happening, and governments are doing their part to support these business-led initiatives to provide standardized frameworks. In Canada, the 2023 Fall Economic Statement solidified the federal government’s intention to introduce legislation establishing a Canadian Open Banking framework. This federally mandated framework would regulate third-party access to consumers’ financial data, paving the way for A2A growth in Canada.

A2A payments make it easier and faster for businesses to reconcile accounts, for consumers to send money overseas, and does its part to ensure that businesses in Canada and the United States do not fall behind as economies modernize worldwide.

Conclusion

Convenience is paramount in today’s world, and this is especially true for payments. As technology has advanced, so have expectations of both consumers and businesses alike. Gone are the days when consumers or businesses are willing to accept the delays in both sending and receiving funds, which is what makes A2A payments such a popular choice.

The rising popularity of A2A payments reflects their ability to meet the changing needs of consumers and businesses in an increasingly digital world. That’s why companies like Flinks are evolving their offerings to include A2A payment methods. As payment methods continue to modernize, having a simplified instant payment process that gives customers options and security is key for businesses to gain a competitive edge. By prioritizing the evolving needs of their customers, businesses can provide a convenient and simplified experience they’ll want to come back to.

.png)