The payment methods a business offers, regardless of their size or industry, can directly impact their ability to attract and retain customers. Convenience is paramount in the modern era— customers expect seamless, secure, and diverse payment options.

Moreover, the right payment methods can enhance cash flow, reduce the risk of fraud, and expand a business's reach. Therefore, understanding and adapting to the changing landscape of payment methods is not just a matter of staying current, but a crucial strategy for business growth and sustainability.

Digital payments are fast becoming the gold standard of payment methods in Canada. Since the COVID-19 pandemic, 43% of Canadians have changed their payment preferences to digital and contactless for the long-term.

Although the pandemic did play a role in the evolution of payments in Canada, there are other factors to consider, such as the introduction of Open Banking regulations in Canada and the increased prevalence of Interac e-transfers. In 2022, Interac e-Transfer reached more than one billion transactions over a 12-month period for the very first time in its 20-year history, with 19% of those transactions involving a business.

Consumer needs are also evolving, with 75% of consumers identifying the importance of receiving payments and having access to funds instantly. With the launch of FedNow, banks and financial institutions of all sizes in the United States are keeping up with the evolving needs of their clients by taking advantage of this new and secure instant payment structure developed by the Federal Reserve.

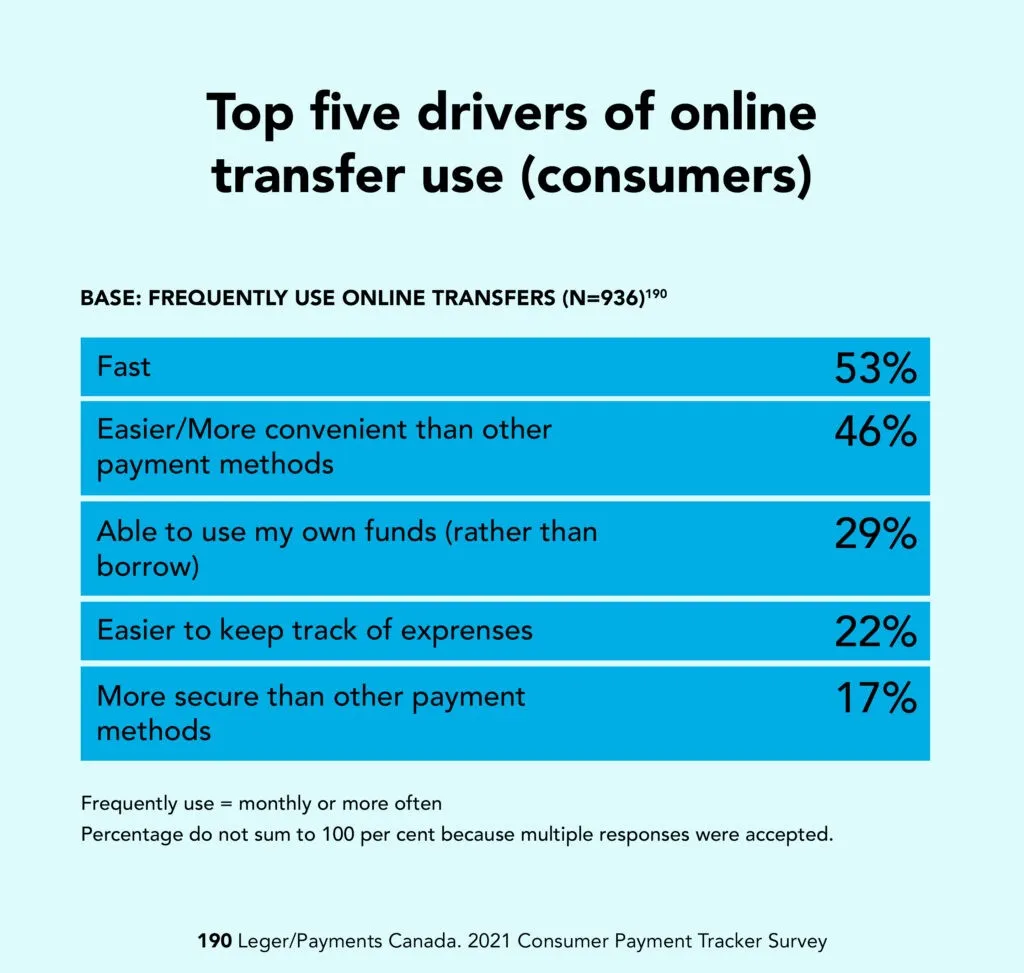

There isn’t a stark difference between the wants and needs of Canadian consumers versus American consumers when it comes to payments. Take a look at the top five drivers for online payments in Canada:

*Source: Canadian Payment Methods and Trends Report, 2022

Convenience and speed are top considerations for consumers in Canada, meaning Canadian financial service providers need to prioritize these factors in order to give their business partners the tools they need to stay competitive. It’s also important to consider which available payment types are best suited for their business needs.

What payment types are available for Canadian businesses & consumers?

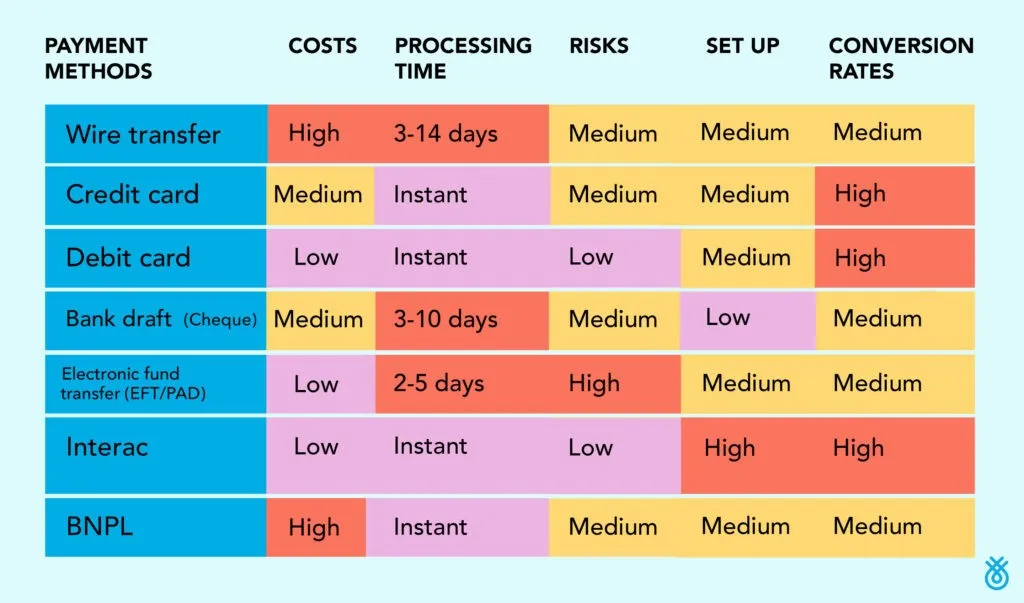

- Electronic Funds Transfer (EFT): This is an umbrella term used globally that includes direct deposit, electronic remittance, pre-authorized debit and other online bill payment transactions. In Canada, this is often referred to as Automated Funds Transfer (AFT). In the United States, this is known as ACH (automated clearing house), which facilitates account to account payments.

- Interac and/or e-transfer: An e-transfer is an electronic payment method of transferring funds between two bank accounts using email, phone number, or account alias and online banking services. In Canada, this is facilitated by an Interac™ e-transfer. An Interac™ e-Transfer is a method for people to transfer money from one account to another electronically.

- Credit card and/or debit card: Credit cards let users borrow money from the issuer to purchase goods and services, which must be repaid with any interest and additional charges, either fully by the due date or gradually. Debit cards allow cardholders to pay for their goods and services directly from their bank account and can be used in place of cash to make purchases.

- Paper: cheque, cash/bill: The traditional method of non-digital payment, cash involves bills or coins paid by the recipient for goods or services provided. Cheques are a written order instructing your financial institution to give money from your account to the goods or service provider that is depositing the cheque. In recent years, cheques can also be issued, processed, deposited and cashed digitally as well.

- Wire transfer: A wire transfer is a form of electronic payment that sends money directly from one bank account to another bank account. The key differentiator and benefit of wire transfers is their ability to remit cross-currency payments internationally. Due to the messaging infrastructure and multi-nodal nature of wire transfers, they are generally costlier compared to other payment methods.

- Mobile wallets: A mobile wallet is a digital way to store credit, debit, ID, and gift cards so that purchases can be made using a mobile smart device rather than a physical card. Apple Pay, Google Pay, and Shop Pay are some top examples.

- Digital currencies: Digital currency refers to a wide range of electronic money. This can include currencies like Bitcoin (and other cryptocurrency), Stablecoins or central bank digital currencies (CBDCs). For most of these digital currencies that operate via blockchain , there is not a single entity controlling the network but rather a decentralized peer-to-peer (P2P) network where the “peers” are those making digital currency transactions within the network.

The challenges of current payment methods

Processing Time

Currently it takes Canadian banks at least one business day to process a payment, even mobile bill payments. When funding a new account, it can take 3-5 business days, which can potentially deter customers during onboarding. If the digital onboarding process takes longer than 20 minutes, 70% of customers completely abandon their attempt to open an account.

Costs

One of the biggest barriers facing businesses with debit or credit card payment methods is the fees associated with each payment type. Transaction fees (including but not limited to interchange fees, service fees, assessment fees, etc.) associated with credit and debit cards on both business and consumer sides can be costly. Although giving customers more choice, businesses are faced with additional setup costs, lower margins, and ongoing fees.

Risks

There are risks inherent with all forms of payments ranging from unauthorized transactions, bounced cheques, counterfeit cash, to data breaches, fraud, phishing, and so on. Mitigating risk to existing payment methods requires significant financial, security, and operational investments. Despite risk mitigation techniques, there remains the potential of financial losses, additional administrative work, and legal consequences to businesses lacking the proper safeguards.

Conversion Rates

Many of the challenges listed above are related to payment processors, this includes delays in payment processing time, customer security concerns, transaction costs for both businesses and consumers, and complicated payment flows. These challenges can make it difficult to convert users into paying customers, which in turn, can impact product adoption rates and make it difficult to increase the long term viability of customers.

Future of payments in Canada

Understanding these pain points and existing frictions in the current state of payments, governments have taken notice and are introducing modern payment frameworks. Currently, the United States has shot ahead of Canada with the introduction of FedNow’s instant payments, along with a rapid path to Open Banking adoption led by the Consumer Financial Protection Bureau.

Canada isn’t that far behind. The federal government is working on its Open Banking framework recommendations and continues to support the development of a real-time rail framework that will transform and modernize payments in Canada. Let’s take a look at what this means for Canadians:

What is Open Banking and how does it benefit Canadians?

Open Banking in Canada has been in motion since 2018, when the Minister of Finance appointed the Advisory Committee on Open Banking. Although implementation is still pending for Canadians, Open Banking frameworks have already been rolled out in other countries such as the UK and Australia.

Open Banking is a secure way to give third-party service providers or applications (3PA) user-permissioned access to banking, transactional, and other financial data from financial institutions (banks and credit unions) through an application programming interface (API). While it’s one of the safest ways to share financial data, it also provides Canadians control over what data they share with 3PAs.

Beyond control and security, there are many benefits that Open Banking provides for Canadian businesses. One of the top benefits is the real-time data transfer from your bank to a 3PA, which is both convenient for consumers while also boosting the efficiency of financial operations.

Take for example accounting softwares and automatic reconciliations. Seamless connections and real-time data syncing save businesses time and reduce manual errors in their bookkeeping, enabling SMBs to have up-to-date views of their financial position.

Another key benefit is the shortening of payment times, an important factor in payment processing for SMBs. 29% of Canadian SMBs say delays in ingoing and outgoing payments are their biggest payment pain point. Open Banking can address this concern by enabling the real-time sync of financial data, which authenticates bank accounts and balances and also has the potential to shorten payment times. In addition, Open Banking encourages competition through product transparency across financial institutions while also reducing manual processes, which results in lower payment fees for businesses.

What are Real-time Rails and how does it benefit Canadians?

In 2016, Payments Canada announced a plan to modernize the Canadian payment system by introducing a new payment rail.

The Real-Time Rail (RTR) payment system allows the request and instant transfer of funds 24/7, along with the ISO 20022 financial messaging protocol that standardizes formatting with higher quality enriched transactional data that reduces errors, facilitates faster reconciliations, and increases the overall usability of transactional data.

Cash flow management was the second leading cause of dissatisfaction with payments for Canadian SMBs. With the introduction of this new system and standard, Canadian businesses will have better cash flow control and improved financial productivity.

What’s next?

Although these plans are in motion, as of publication, they have yet to be implemented. Open Banking, for instance, was projected to be available by January 2023, but has unfortunately been stalled. The most recent update has been the confirmation of Abraham Tachijian’s term as Open Banking lead being extended, but that announcement did not include any updated implementation timelines. For RTR, plans to deliver the new rail are still ongoing, with Payments Canada providing an update of its delays without providing a clear expected rollout date.

Waiting for their implementation doesn’t mean Canadian businesses are standing still. Companies such as Flinks are taking this opportunity to prepare for their eventual rollout, with solutions that are built for Canada’s current Open Banking environment while still being adaptable to impending regulatory changes.

.png)