How to drive more user conversion on fintech?

People know what fintech companies have to offer and are jumping on board. An outstanding 96% of consumers worldwide are aware of at least one money transfer and payment fintech service, according to the 2019 Global FinTech Adoption Index. Likewise, 64% of global consumers have adopted fintech into their financial management routines and systems.

Despite this success, only 46% are willing to share their bank data with other organizations.

When asked to verify and connect their bank account information to digital platforms or apps, users drop off. Among fintech adopters, 71% of them worry about the security of their personal data when dealing with companies online — that’s more than non-adopters (at 65%). Security, however, is only a minor part of the perceived problem.

Digital banking connectivity is a widespread challenge and a massive opportunity with the right tools.

Why consumers fail to verify their bank accounts

- Lack of digital finance awareness and comfort

- Misunderstanding of digital security measures

- Complex digital onboarding

- Unclear value proposition

- Flawed user journey

Fintech is here, but are consumers ready to embrace it?

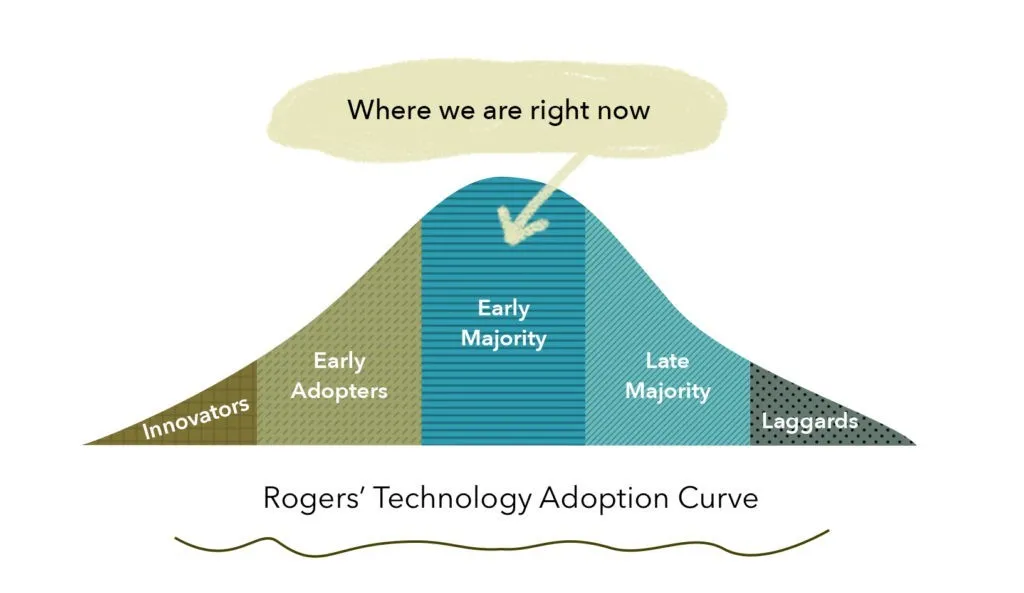

To fully understand the challenges and opportunities that fintech companies face, we must first consider finance’s adoption curve challenges in the past. All innovation follows an adoption curve. Innovators and early adopters are first on board with new technologies, followed by the early majority, late majority, and then the not-so-tech-savvy laggards.

Many consumers are becoming familiar with fintech products and services and are seeing results from sharing their financial data with financial wellness apps, digital lenders, and so on. For example, 3 out of 4 global consumers already use a money transfer and payments fintech service, while 1 in 2 uses a fintech insurance service.

However, digital adoption in finance has been historically slow and challenging.

This is especially true on the consumer side where the adoption curve is slower than that of financial enterprises.

Credit and debit cards are a great example as they used to be made of paper. People were slow to adopt plastic and get used to magnetic strips and electronic chips. This is despite the now-obvious security risks of containing so much bank information on a piece of paper, not to mention digital convenience.

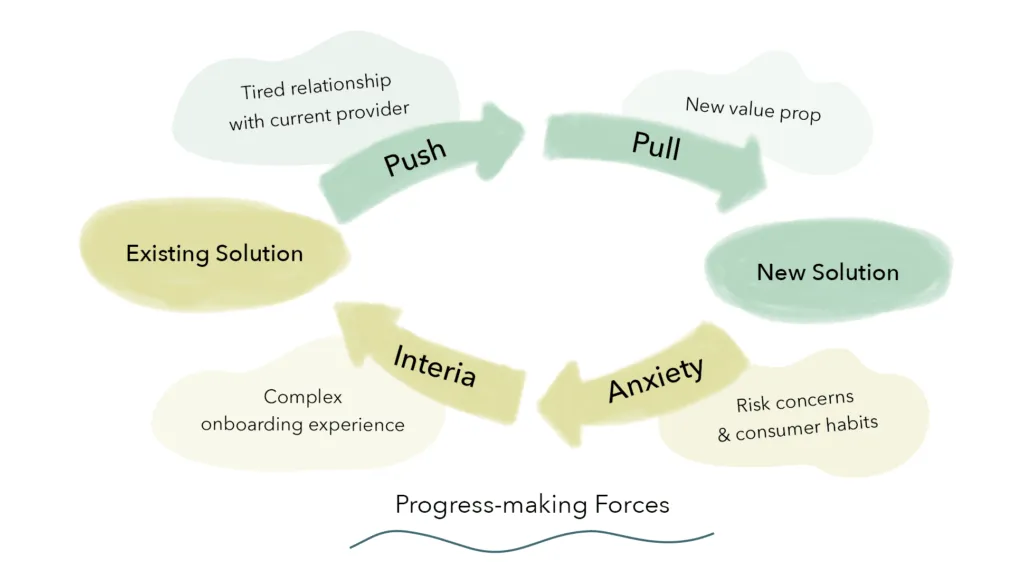

Every process in finance that hasn’t undergone digitization now seems cumbersome, time-consuming, unsecure, and ineffective. However, to fintech adopters and non-adopters alike, the digital alternative must be more secure, effective, efficient, and frictionless than its traditional counterpart. Otherwise, when an app asks a user to share banking information, it will likely trigger a resistance.

5 common reasons consumers fail to verify their bank accounts and how to fix them

1. Lack of digital finance awareness and comfort

The challenge:

Linking their bank accounts to a service provider could be a sensitive issue for customers who are new to digital finance. For example, 22% of non-adopters stick to their incumbent financial institution because of a greater level of trust than with fintech newcomers. Likewise, 34% of non-adopters are not aware or have a limited understanding of how fintech challengers work. As with every new experience, there may be a varying lack of awareness and comfort, especially when it comes to sensitive banking information.

Our advice:

To shift your customers’ mindset and embrace fintech, consider thorough communications leading up to asking them to verify their bank accounts. Make sure that any potential concerns or pain points have been addressed clearly before jumping on their financial data. And remember to talk to your customers without technical jargon so that they can truly understand and buy into your offerings.

2. Misunderstanding of digital security measures

The challenge:

Different consumers have divergent levels of understanding of digital finance, hence divergent levels of security concerns. Compared to non-adopters, tech-savvy adopters can be more worried about revealing their usernames and passwords. And sometimes, they can misunderstand that a service provider can have direct access to their bank balance once they link their accounts.

Our advice:

To address the disinformation and confusion around access security, explain what digital security measures are in place for their account protection. Simply put, lots of digital finance businesses use bank-level encryption or advanced encryption standards to make sure that no one can have direct access to a customer’s bank account.

3. Complex digital onboarding

The challenge:

If your end-users get lost in the digital onboarding process, they may lose sight of why they came to your product in the first place — and no longer want to verify their bank accounts.

Imagine your users can’t find their bank on the list provided within the system, or they have a difficult time navigating the connection flow. Suppose that there are too many steps, or the onboarding process takes too long — and they’re unclear how far they are along the way. The same goes if they are asked to verify their bank accounts too soon.

Our advice:

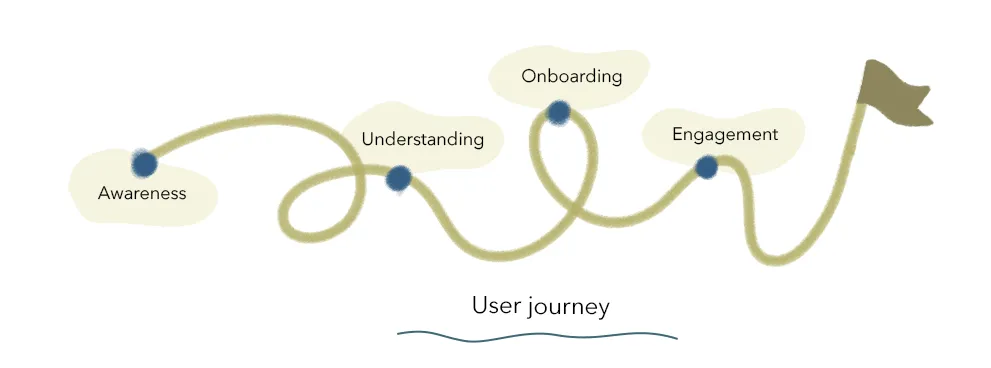

Examine all the touchpoints consumers have with your brand before their onboarding. And ask yourself, is their onboarding experience simple, frictionless, and pleasant? Do you engage with them on every channel with the right messages? How much trust has been established between you and your customers before asking them to link their bank accounts?

4. Unclear value proposition

The challenge:

In the same vein, how clear is the reward on the other side of the onboarding? In the digital lending space, for example, 70% of consumers are willing to provide additional financial data to lenders if it increases their loan approval chances or improves their interest rates. If your end-users don’t understand what’s in it for them, they may begin to question whether all of this is necessary or how their financial information will be used.

Our advice:

Keep in mind the top reasons why consumers switch to fintech service providers: convenience, faster turnaround times, and lower fee policies. And explain to them how digital connectivity can lower costs and optimize offerings by reducing manual efforts, eliminating data entry errors, and providing more personalized recommendations. Articulating your value propositions in concrete ways can increase the legitimacy to verify your customers’ bank accounts and boost their confidence in you over other financial incumbents.

5. Flawed user journey

The challenge:

Lastly, end-users may have encountered UX problems during the digital connection flow and aren’t prepared to take some necessary steps to get on the right track. For example, technology issues such as long responsive time and broken links, complicated user flow with too much back and forth, and poorly designed error handling can drive your customers away from verifying their bank accounts.

Our advice:

When paying attention to end-users’ opportunities, don’t overlook their frustrations throughout the user journey. Starting by fulfilling their smallest needs can make a huge difference. While there is no single definition of good user experience, your customers are accustomed to mobile-first workflows, near-perfect system uptime, pre-filled data fields, and a certain degree of control over their experiences, such as a save feature within the system. These efforts can enable your customers to quickly pick up where they left off and happily re-engage with you.

Understanding customer pain points is the key to succeed in digital connectivity

Digital connectivity is an utmost concern to fintech businesses. At Flinks, we’re constantly working with and learning from our clients to ensure that they are set up for success. With your business needs in mind, we offer comprehensive connectivity models and tailored solutions to maximize end-user conversion and increase your service quality.

Leveraging your users’ financial data in your products and services will ultimately build your competitive advantage and increase your brand value. Talk to our experts today and let us help your business thrive.