Access to financial data has become table stakes in the industry. As a leading provider, we’re seeing millions of consumers adopting data connectivity as the new default option to share their financial information.

Data connectivity puts consumers in control. In exchange for their financial information, they can activate apps and services instantly, get more visibility than ever over their finances, and use a slew of new products to achieve their goals.

This has accelerated the pace of innovation for all players, from established banks to new fintechs—and has kept raising the bar on consumer expectations. Access is essential, but it’s just a start. So what’s next?

Read up our highlights below, and download our full whitepaper for the complete analysis.

Key Takeaways

- Data is the oil of our time. Just like oil-powered combustion engines made modern life possible across large geographical spaces, data-powered software engines allow billions of individuals to interact and transact in digital spaces.

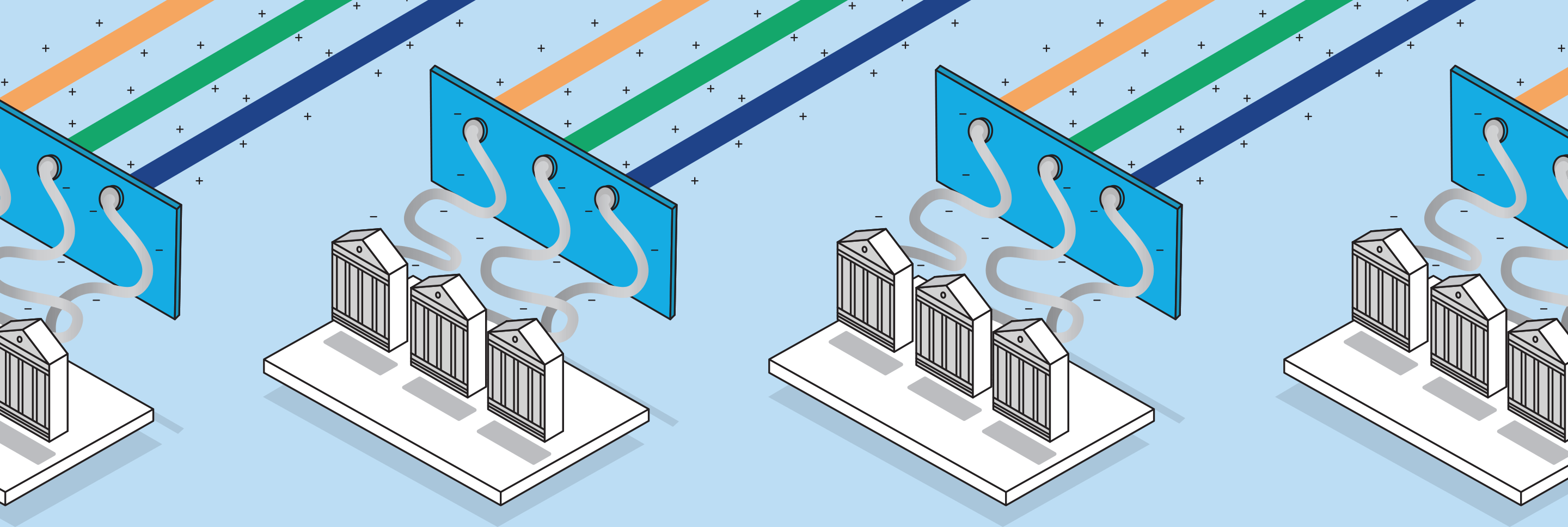

- Financial businesses have been served with only one type of data enrichment products based on the categorization of spend. This leaves out a wide range of business processes that could be powered by enriched data.

- Flinks pioneers a new generation of data enrichment tools that make it easy for businesses of all sizes to extract insights from their customers’ financial data, and use them to power their use cases.

- This benefits businesses all across the industry: Lenders, fintechs, banks, and more.